Western Australia’s Wholesale Electricity Market (WEM) operates across the South West Interconnected System (SWIS), which supplies electricity to over 1.1 million households and businesses in the south-west of Western Australia. The WEM is undergoing radical transformation to accommodate the deployment of renewable technologies. On the supply side, there is a need to progressively replace the existing coal fleet over the next decade; on the demand side, there has been, and is expected to continue to be, strong growth in consumer energy resources such as rooftop PV and batteries.

Replacing the existing coal fleet with rooftop and utility-scale solar power, and also onshore wind power, requires extensive energy storage solutions to firm the supply, due to the intermittent nature of variable renewable technologies. More generation capacity is also needed to meet the electrification-driven increase in electricity demand projected over the next three decades.

Incentivising investment in these technologies and maximising the benefits to consumers from these investments, requires changes to the design of the WEM as well as to how electricity networks are planned and economically regulated. We see similar trends and requirements in other electricity markets globally.

Baringa’s WEM Reference Case provides an independent perspective on the demand and supply-side changes in the WEM, drawing on information from public sources as well as Baringa in-house views. This provides projections of black and green prices, reserve capacity prices, and capacity and generation mixes.

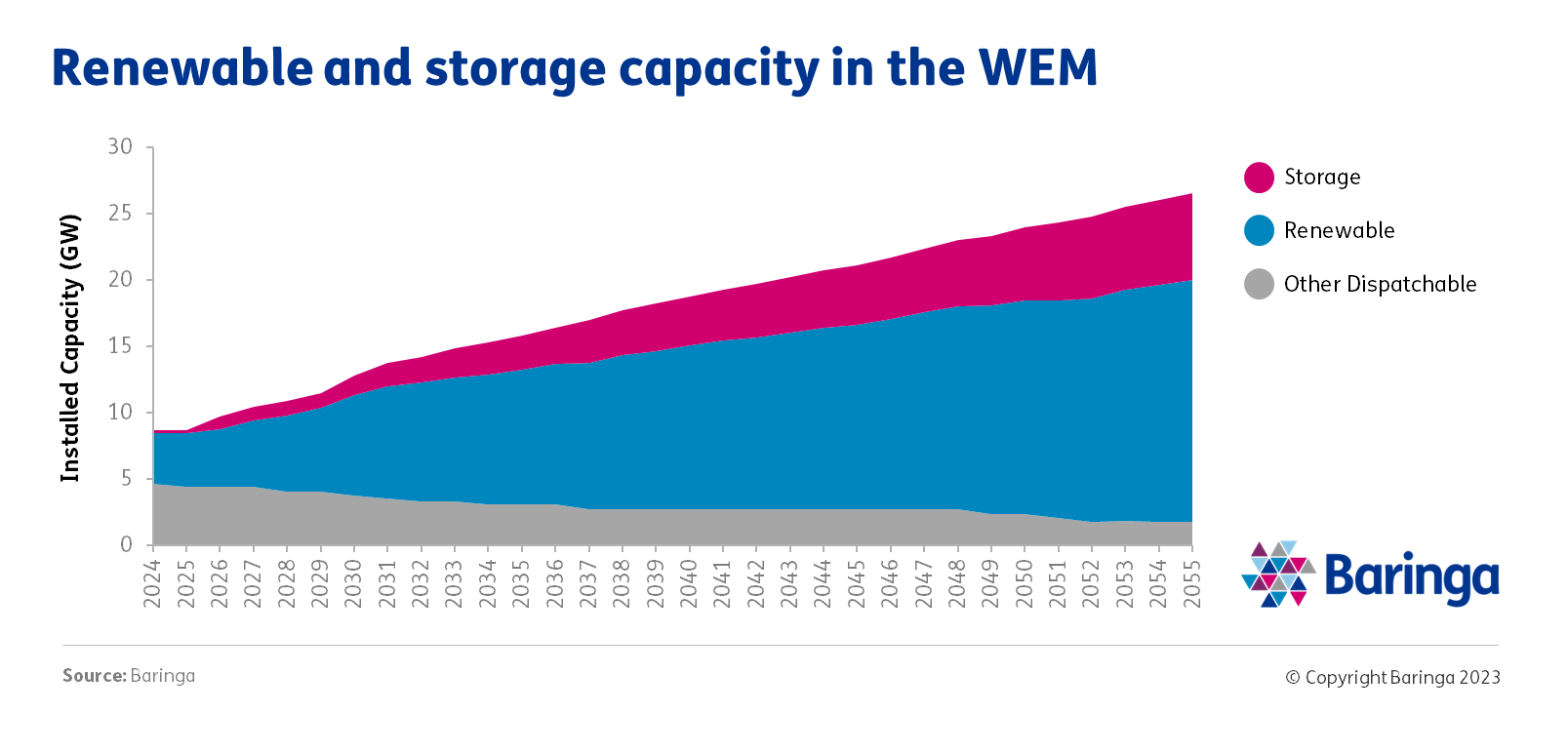

Renewable and storage capacity in the WEM will increase by six times today’s levels. What’s driving this?

The WEM Reference Case projects renewable and storage capacity in the WEM to increase to 25 GW by 2055, almost triple the existing capacity.

Renewable and storage growth will be enabled by 3 key factors:

- Earlier exit of coal plants

- Electrification-driven increase in demand

- Ongoing and newly announced market reforms

The exit of coal will result in a substantial reduction in overall supply capacity, creating the investment opportunity for 5GW of renewable and storage capacity by 2031

In June 2022, the WA Government announced the closure of all government-owned coal plants by 2030, as part of transitioning the State towards net zero emissions by 2050 and achieving its economic development goals. The announced closures are up to fifteen years earlier than the plants’ technical lifetimes.

This represents a substantial loss of 1.4 GW of dispatchable capacity and annual generation of around 7 TWh from the SWIS. Based on our WEM Reference Case this creates the investment opportunity for the economic entry of 5GW of utility scale renewable (wind and solar) and storage capacity by 2031. It also requires significant investments in the transmission network as the new renewables are (and typically will be) in different areas to the coal plants.

Electrification of heavy industry creates new offtake opportunities for renewable and storage development, and creates additional requirements for transmission investment

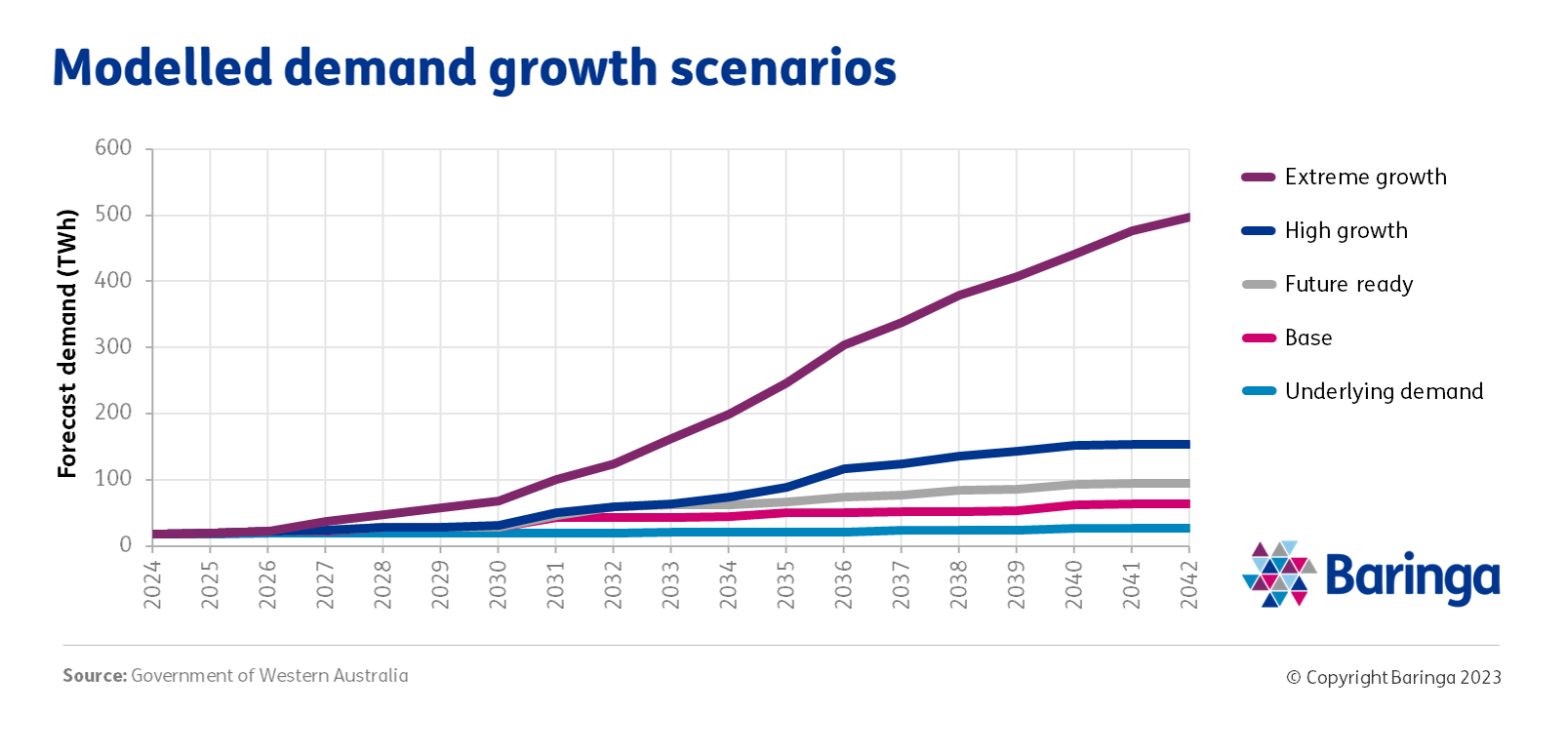

Both the WA Government’s SWIS-Demand Assessment (SWIS-DA) and AEMO’s Electricity Statement of Opportunities (ESOO) 2023 project strong electrification-driven growth in demand.

Of the five scenarios in the SWIS-DA (see chart below), the Government of Western Australia selected Future Ready for further development, as it provides a balance between short-term needs and long-term network options. Under this scenario, demand in the SWIS reaches five times today’s levels by the early 2040s.

If realised, this scale of growth will be unprecedented for the WEM. And it’s worth noting that Future Ready isn’t the most aggressive of the five SWIS-DA demand scenarios. This demand growth has implications for investment in the WEM.

Offtake opportunities for new renewable and storage developments

The electrification of existing energy-intensive industrial demand, alongside emerging industries including green hydrogen production, will create strong growth in energy consumption and peak demand. This is driven by WA and Federal Governments’ emissions reduction targets, including the commitment to reducing emissions by 43% by 2030, and a net zero target by 2050.

This level of growth is also anticipated to create significant opportunity for renewable energy and storage developers seeking revenue certainty via two routes-to-market:

- Corporate Power Purchase Agreements (PPAs): For consumers with growing loads via electrification, who may not have as much expertise in managing electricity procurement, long-term renewable energy contracts represent an attractive avenue to creating long-term cost certainty while also making progress towards decarbonisation ambitions.

- Retailer-offtake: As the state retailer Synergy loses progressively larger amounts of existing capacity, renewable energy offtake contracts represent a means to bolster energy supply for its diminishing retail hedge book.

For both offtake avenues, supplying physical (e.g., tolling agreements, firmed renewable supply agreements) or financial contracts (e.g. caps, swaps) backed by energy storage can provide significant value in managing electricity market risks while providing additional revenue premiums to suppliers.

This opportunity is highlighted by the tripling in installed generation capacity in the WEM (see first chart above). The growth in utility scale storage is mainly of 4-hour duration, which is in line with recent battery announcements by Neoen and Synergy.

Challenges to Transmission investment will drive an increasing focus on the location of new generation and storage projects

The SWIS-DA estimates over 4,000km of new transmission lines will be needed to service the demand projected under Future Ready. However, it’s unclear how the extent of transmission investment planning implied by the SWIS-DA demand projections can be delivered, and who will fund this investment.

These concerns were expressed publicly during the recent Energy in WA conference as well as privately to Baringa experts in various stakeholder conversations with clients in Perth. As such, the timing of Future Ready is considered a significant challenge by many market participants.

A lack of investment in transmission infrastructure may delay the electrification of other sectors and the investment in new generation and storage projects. It will be increasingly important to assess where generation and storage projects connect to the network to avoid the risk of significant transmission congestion.

Ongoing and recently announced market reform should be watched closely by investors

Investors will be keenly monitoring the impact of coal closures and demand growth on the market to identify new investment opportunities. They should also be alert to upcoming market reform and state government policy announcements to identify indicators of further risks and opportunities, namely:

- One of the key changes in the upcoming WEM Market Reform program, with implementation this October, is the move to a security-constrained economic dispatch (SCED) mechanism in the real-time Balancing Market. Whilst this poses risks for investors in the form of uncompensated curtailment, there are opportunities for storage projects to be paid for alleviating the congestion faced by other (generation) projects.

- The introduction and co-optimisation of Frequency Co-Optimised Essential System Services (FCESS), which will serve to more transparently price and schedule system services. This will present a new revenue stream for utility scale battery projects and flexible gas assets. Baringa provides curtailment and FCESS projections for SWIS-connected generation and storage projects, as part of our WEM market advisory work. The introduction of SCED makes such projections even more important for project developers and their financiers.

- The recent Reserve Capacity Mechanism (RCM) review broadly retains the existing elements of the RCM, whilst announcing that a new limb will be added to the Planning Criterion to meet steepest operational ramp periods using a new ‘flexibility product’. This presents an opportunity for eligible fast-ramping battery storage projects to earn greater than previously anticipated capacity payments.

- Accompanying the recent SWIS-DA was a package of proposed reforms for more coordinated transmission planning and greater certainty for renewables and storage investment. These policies present the potential to better deliver network connections for new projects, encourage low-emission dispatchable capacity, and guarantee wholesale revenues for firmed renewables.

Baringa has supported investors in both the NEM and the WEM on over 100 project financing transactions to date. We help our clients to identify which technologies to invest in, the locations with the most potential, and the optimum timing of entry. Find out more about our WEM Reference Case, and the risks and opportunities for investment, by contacting one of our experts below.

Related Insights

Next steps for the UK renewable energy industry

Join us for this webinar where we’ll be discussing the impact of recent developments on the UK’s Contracts for Difference (CfD) subsidy scheme.

Read more

European power markets: Navigating the new normal and looking to the future

How will the power markets evolve in 2024 and beyond? Watch the playback of this webinar to access our analysis.

Read more

Financing the energy transition in a volatile market

We examine the recent disruptions that have affected the financing of renewable energy projects in Europe over the past 18 months.

Read more

India’s complex and rapid energy transition presents major opportunities for investors

Baringa's India Reference Case provides a comprehensive overview of the Indian power market and an independent perspective on the demand and supply-side changes.

Read moreRelated Case Studies

Shaping a self-generation strategy for a major data centre

How do you develop an energy generation plan that balances sustainability with commercial due diligence?

Read more

Evaluating the case for the world’s biggest offshore wind project

We helped our client reach financial close for all three phases of the project, securing 15-year CfDs with delivery between 2023-2025.

Read more

Green Hydrogen value-chains unpacked

Mapping and analysis of the potential of Green Hydrogen across multiple European markets helped our client’s strategic focus and investment decision-making.

Read more

Working with Netbeheer Nederland, we helped the Netherlands’ grid get to grips with solar

New solar panels are installed across the Netherlands daily. Each one is a step towards a greener energy system but only if that system is set up to use them.

Read more