What is a financial Power Purchase Agreement?

A financial PPA, or virtual PPA, does not involve the physical sale or purchase of electricity. It is an agreement between a renewable energy generator and a corporate buyer where:

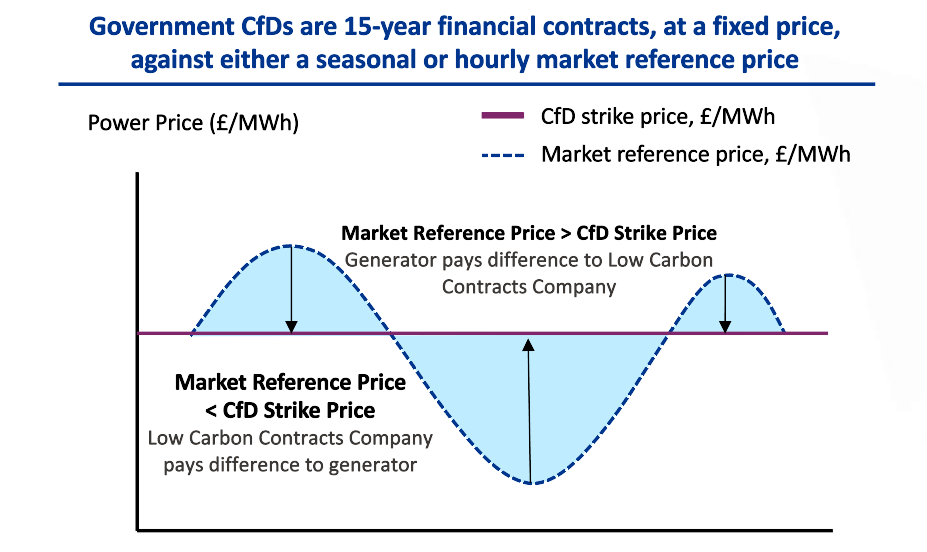

- The two parties agree on a fixed “strike price”

- If the market price for electricity at the time of generation is higher than this strike price, the generator pays the difference to the buyer

- If the market price is lower than the strike price, the buyer pays the difference to the generator

This provides both parties with a price hedge, under the assumption that they physically sell/buy electricity at the same market price as the one used to calculate the difference payments. In reality, the hedge will be a “proxy hedge” from the perspective of the buyer. This is firstly because the generation profile of the renewable asset will not match the consumption profile of the buyer, and secondly because the market price used to calculate the difference payment will often not be the same price that the buyer actually pays for physical power.

Despite the lack of physical sale and purchase of power, the buyer will typically obtain the renewable energy certificates as part of this deal, contributing to decarbonising their scope 2 emissions.

Where are they used?

In some markets, regulation means that physical PPAs are harder, or even impossible, and therefore financial PPAs are used. There are circumstances where financial PPAs make more sense: where a corporate buyer has physical demand across several markets with operations across Europe they may opt to sign a smaller number of financial PPAs in one or two markets, to cover the demand across a bigger region instead of signing physical PPAs in all markets. This opens up a new category of risk, called “basis risk”, which occurs due to differences in market price in the PPA markets vs the markets where the buyer has physical demand.

Another, simpler reason corporates may opt for financial PPAs is to avoid complexity associated with buying intermittent physical power. Renewable energy assets generate intermittently due to wind and solar conditions, and this will almost never line up exactly with the demand required by the corporate buyer. Managing this mismatch requires contracts and processes which are more complicated than traditional electricity supply.

Why are they increasingly being used?

Going forward, there are several reasons that may drive corporates to increasingly opt for financial PPAs:

- To more efficiently decarbonise scope 2 demand in smaller markets:

As companies look to more fully decarbonise scope 2, they will often encounter situations where signing physical PPAs for all physical demand doesn’t make sense. Financial PPAs offer a more efficient route to sign fewer, larger PPAs. - To take a “carbon matching” approach to scope 2 accounting:

Where demand is already located in a relatively low carbon intensity market, companies may opt to sign PPAs which bring new renewables online in markets that really need them (i.e. where new renewables can displace coal or other high carbon intensity technologies). Read The Coporate Catalyst, a study commissioned by Amazon for more on this.

How does this impact you?

By increasing your exposure to these contracts, your finance and accounting functions need to get on top of managing them.

Financial PPAs are classified as financial instruments, and their fluctuating fair value needs to be reported on the balance sheet. Balance sheet volatility, driven by changing power prices, causes headaches for CFOs, therefore, the right valuation method is critical: it must pass audit scrutiny whilst minimising balance sheet volatility. This is a challenge because most companies signing PPAs aren’t energy experts. Building internal teams to handle these complex valuations is time-consuming and costly.

If you want to decarbonise your organisation by using financial PPAs, you need to get on top of the balance sheet implications and audit requirements. Clients have been coming to us when it becomes an issue, often because auditors are not accepting valuations or CFOs are becoming concerned about excessive volatility. We can enable you to get on top of this and avoid those issues, get in touch to find out more.