How to unlock the multi-billion dollar e-waste opportunity

8 min read 6 February 2025

Why Book and Claim insetting models can be the answer

On average, the world produces approximately 62 billion kilograms of e-waste1. Businesses now face increasing regulatory pressure to reduce their environmental impact (like CSRD and EPR in Europe) while also trying to find new sources of value in a chaotic economic climate.

Our previous article, Value left on the table with circularity. Could an insetting revolution be the answer? explored how insetting can help tackle e-waste and cut Scope 3 emissions. The key is pairing insetting with a reliable book and claim system to unlock value, decarbonize supply chains, and accelerate the circular economy. Here we explore how such a model can work, and the value it would generate to all stakeholders.

Fundamentals of a combined insetting and Book and Claim model

Insetting: This involves reducing or removing greenhouse gas emissions within a company’s own value chain by investing in suppliers’ initiatives and capabilities.

| How other industries do it: Meta has invested in decarbonizing its data centre value chain by providing financial support to CarbonBuilt, a low-carbon concrete supplier. This investment helps scale CarbonBuilt’s capabilities, benefiting not just Meta but the entire value chain2. |

Book and Claim: The book and claim model allows the sustainability benefits of a physical product to be decoupled and sold separately. This creates a new revenue stream for the producer while providing access to sustainable products or claims for the buyer. A producer generates a sustainable product and records the carbon benefit using an independent register – ‘booking’ it. A buyer can then purchase and ‘claim’ these benefits without needing to produce or purchase the original sustainable product.

| How other industries do it: 123Carbon provides a platform that enables companies to recover the costs of their decarbonization efforts by creating environmental attribute certificates (EACs). These certificates are then sold to freight owners and cargo operators, allowing them to claim verified CO2 reductions in their supply chains3. |

Both practices apply across various e-waste categories, from laptops to data centres, and support decarbonization across the entire value chain. In this article, we explore two specific mobile handset scenarios to illustrate how different value chain players can drive decarbonization while building high-value circular businesses.

Scenario 1: OEMs and recycling enhancement. This scenario focuses on OEMs, which have the final say over product design and can directly influence their upstream supply chains. However, their ability to impact the broader industry is somewhat limited due to their upstream positioning.

Scenario 2: Network Providers and refurbishment loop. Network providers typically have less direct control over product design. However, due to their extensive supplier and partner networks and close connections with customers, they can exert significant influence across the value chain, both upstream and downstream.

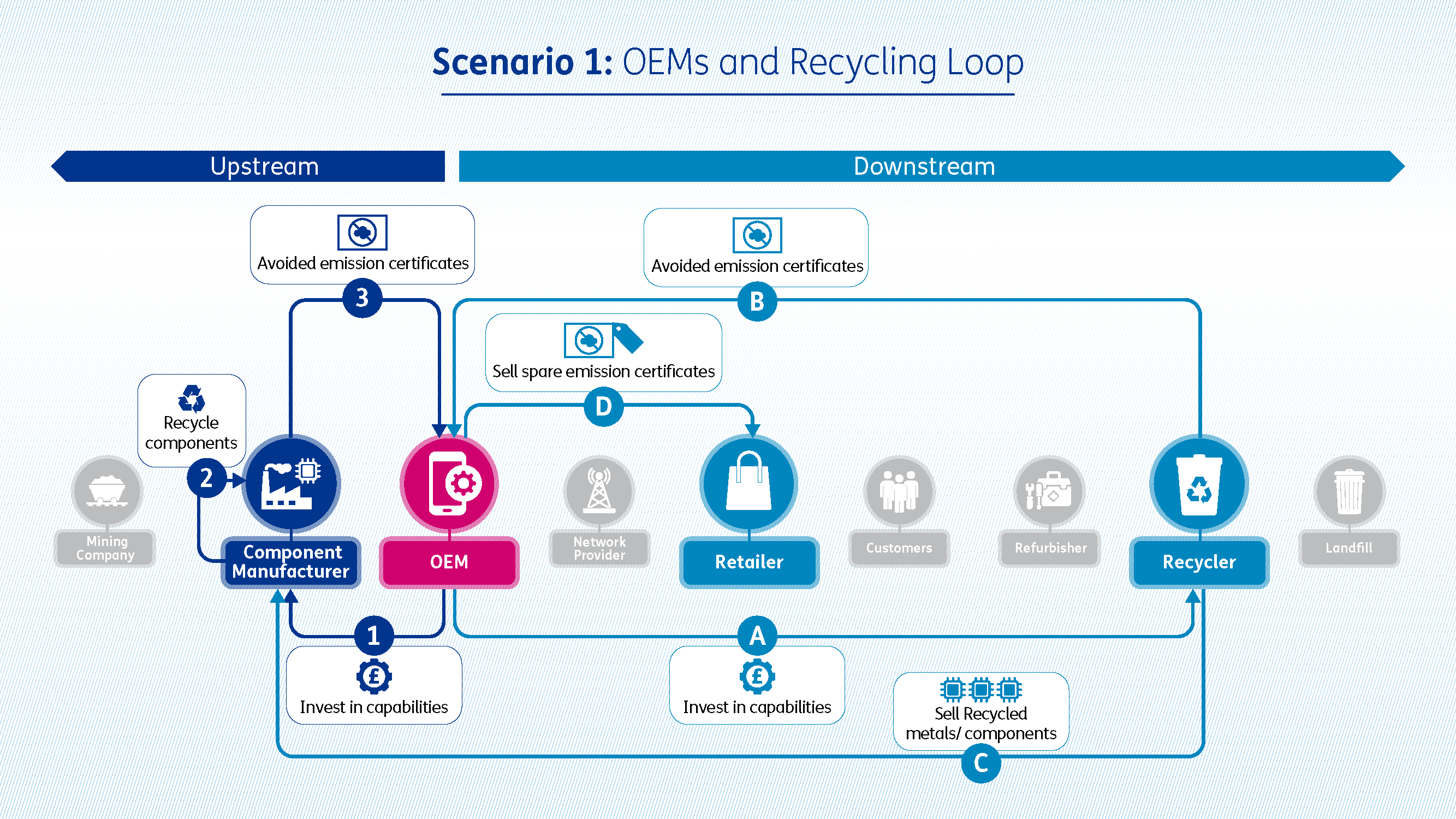

Scenario 1: OEMs and recycling loop

Our first example looks at a hypothetical OEM which invests in upstream handset component manufacturers and downstream recyclers to create circular products.

The OEM engages their value chain partners to create a circular business model. In the first value flow (1 in the diagram above), the OEM works with its component manufacturers to design products that are easier to recycle and retain value for longer. Given that the average smartphone’s carbon footprint is between 60–85 kg CO2e, with over 80% of the emission produced during manufacturing, this is the ideal area to drive down emissions4.

The component manufacturer, in turn, invests in decarbonizing its products, for example by using recycled materials (2). The emissions reductions from these efforts are recorded (‘booked’) and in turn benefit the OEM, as they receive lower-carbon products. Additionally, the component manufacturer can generate emission reduction certificates for carbon reductions associated with products sold to other customers. The OEM may also be able to claim these reductions based on the terms of its initial investment (3).

These could be tied directly to the original project invested in, or from a wider pool of sustainability initiatives. All claims and certificates should be audited by a third party and recorded and allocated on a public register ensuring transparency, authenticity, and immutability.

| Apple has been working with manufactures such as Alcoa and Rio Tinto to purchase carbon-free aluminium for its handset housing5. |

Similarly, the OEM could invest in a downstream recycler (A) and connect them with its upstream component manufacturing partner. This investment would enable the recycler to enhance its capabilities and expand its business by selling recycled assets back up the value stream (B) or to other businesses, thereby driving carbon reduction across the value chain. Depending on the agreement, the OEM could receive certificates (C) from the recycler, either to claim itself or to sell to other value chain partners, such as retailers (D), allowing them to claim the Scope 3 reductions.

| The global electronics recycling market was valued at US$48 billion in 20246. |

Circular models can be a key driver for pricing premiums for OEMs:

- More valuable certificates: Through their control over design, OEMs can control the entire circular process for their products alongside their partners and generate higher quality and more valuable carbon certificates.

- Premium products: OEMs can create premium products that warrant higher prices by designing circular products and investing in supply chains that can repair and recycle these products. As in other industries (eg used cars) creating a strong secondary market for used products at the end of their ‘first life’ drives residual value and in turn upholds price premiums for new products.

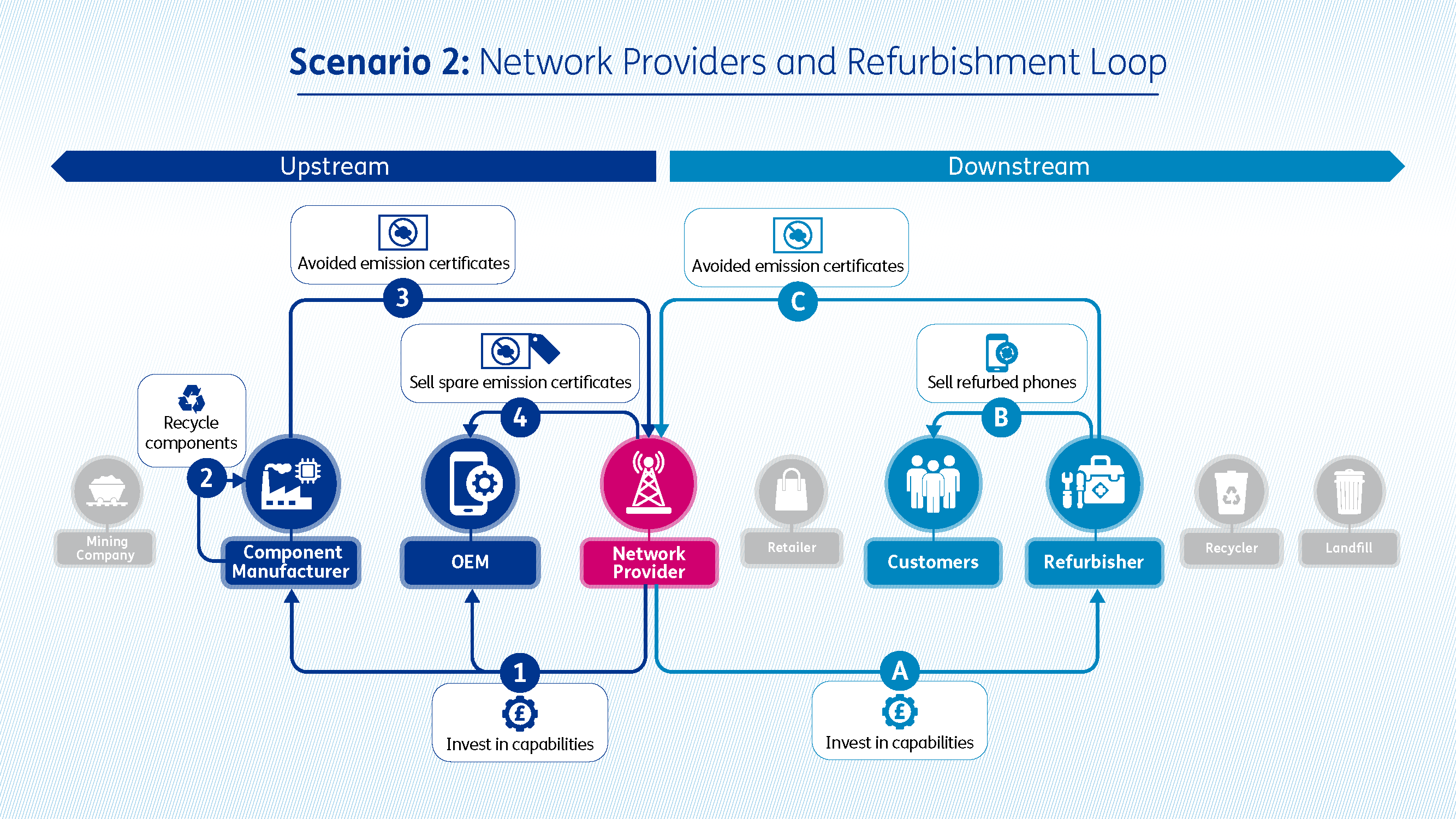

Scenario 2: Network Providers and refurbishment loop

Our second scenario looks at network providers, and how they can work with upstream OEMs and component manufacturers as well as downstream refurb businesses to drive the circular economy and reduce emissions in mobile handsets.

A network provider could invest in a component manufacturer or OEM partner (1) to enhance circular capabilities or support design changes that reduce their supply chain partner’s Scope 1 and 2 emissions. As in Scenario 1, independently validated emissions reductions can be passed back to the network provider as Scope 3 certificates (3). Any spare certificates can be sold by the Network Provider to others in the Value Chain (4).

Given the growing second-hand market, the network provider could also invest in a refurbishment business (A). This investment would enable the refurbisher to scale operations and sell more second-hand or refurbished phones, thereby reducing the need for new handsets (B) and generating avoided emissions. If independently validated, these avoided emissions could be translated into Scope 3 avoided emissions certificates for the network provider (C). The refurbisher could also sell any surplus certificates to other network providers or retailers, as can the network provider.

Circular models can be a key volume driver for network providers:

- Extensive customer base: Provides a large potential pool for embedding circular economy activities. Network providers could stimulate generation of avoided emission certificates directly by encouraging customers to buy refurbished devices.

- Vertical integration: Network providers can capture more of the value by integrating refurbishment capabilities into their businesses – for example through devices collected and resold through its trade-in and upgrade programs. This would also build closer connection with customers and provide better control over second-hand asset value.

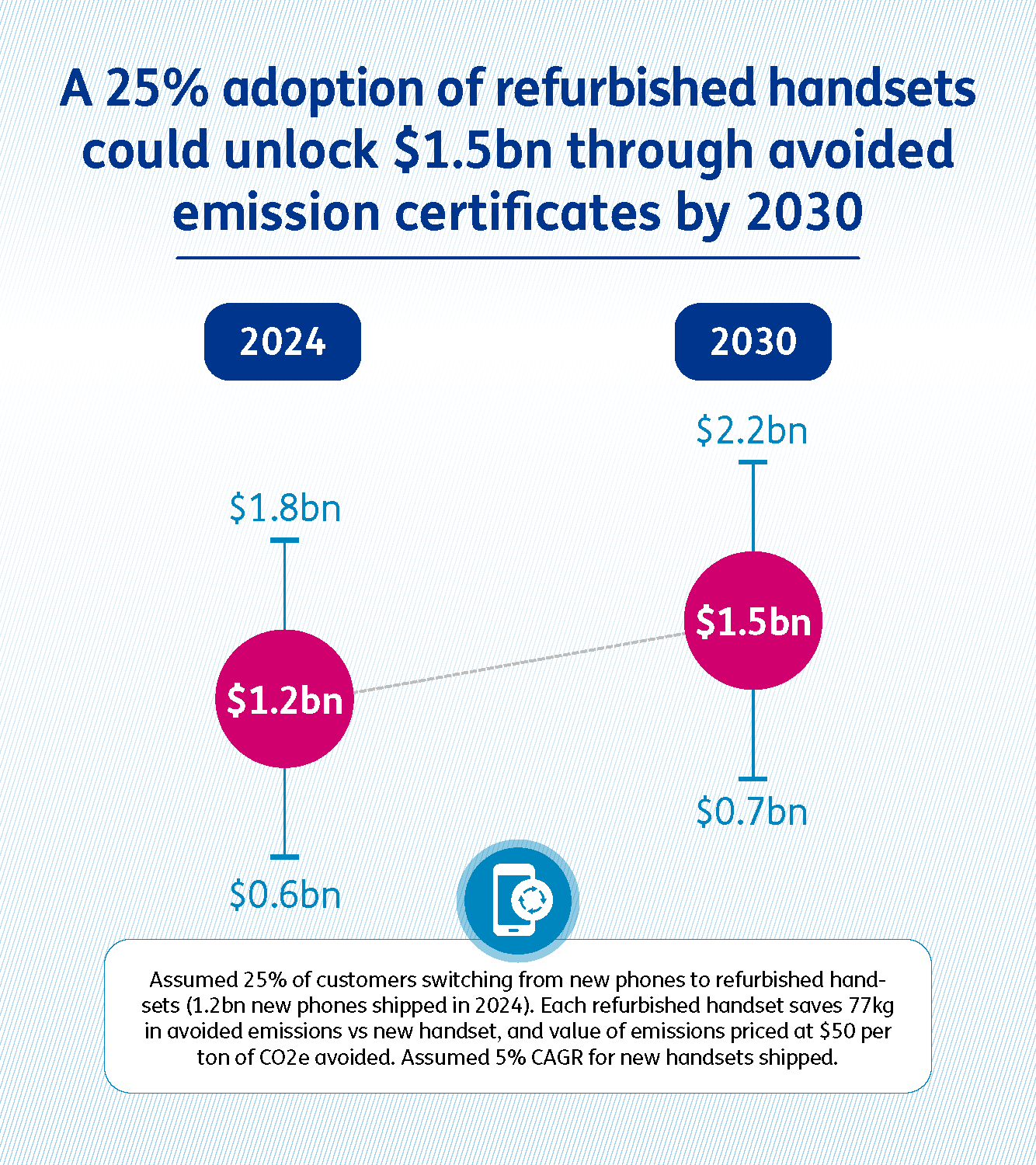

| The refurbished smartphone market is estimated to be US$80 billion in 2024. In addition, we estimate that the value of avoided emission certificates could be around US$1.5 billion by 2030. |

Conclusion

This remains a nascent but promising area of value creation for all e-waste value chains. The scenarios outlined are just two narrow examples of how insetting and book and claim models can be leveraged to build high-value circular businesses and decarbonise value chains.

Clear benefits for investors

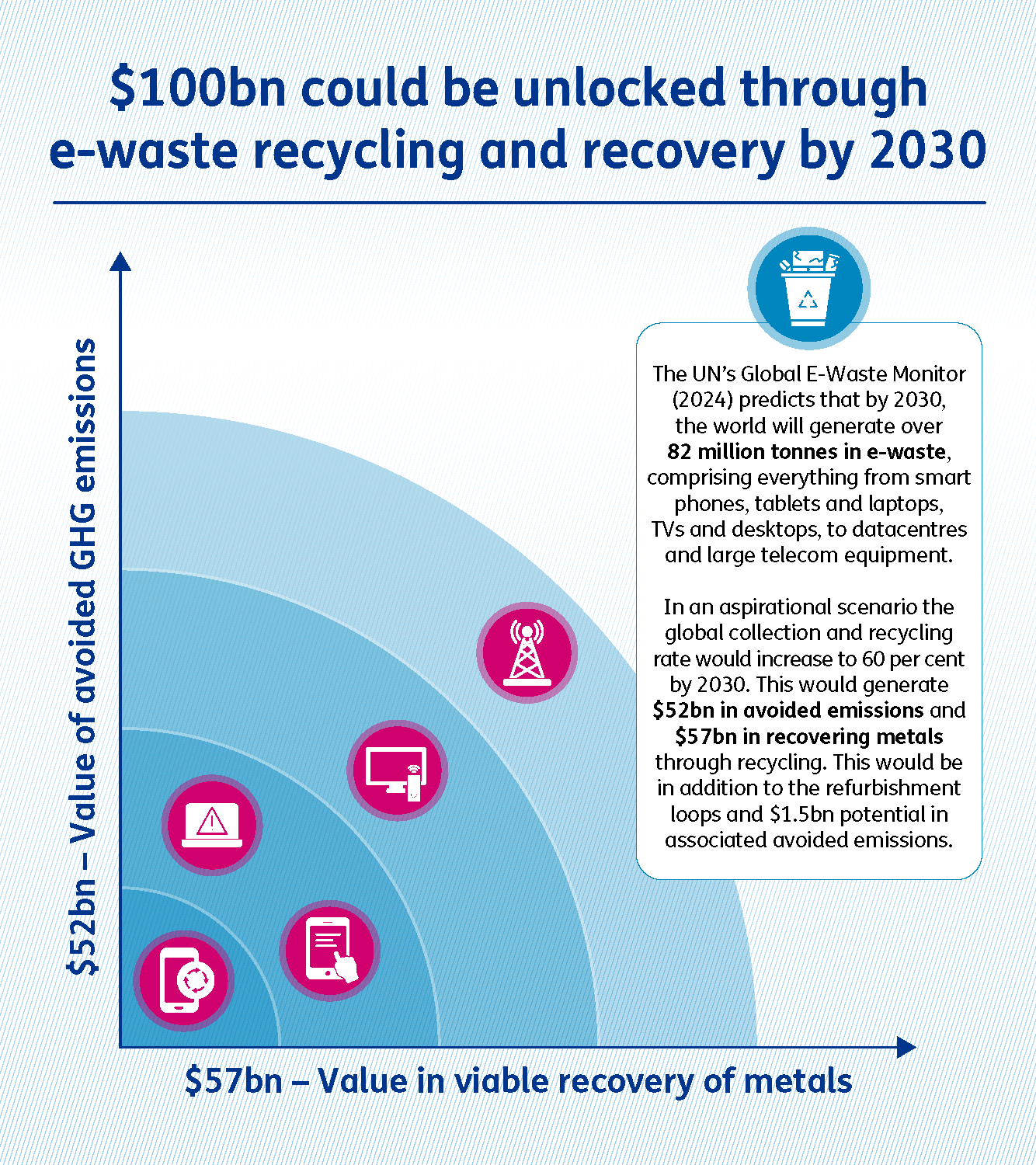

This model presents a meaningful way to reduce Scope 3 emissions while unlocking significant financial opportunities. Monetizing refurbishing, recycling, and reuse activities through independent certification or registration of reduced and avoided emissions creates additional revenue streams. Moreover, insetting certificates have the potential to command higher valuations than external carbon offsets, due to a lower risk premium. Combined, this could achieve a healthy return on invested capital in the circular economy. Within the next 5-10 years, as refurb adoption and recycling rates increase across the industry, the potential value unlock across all e-waste could climb to over US$100 billion.

Beyond financial incentives, insetting activities allow companies to directly control and demonstrate emissions reductions within their supply chains, mitigating brand risk compared to alternative mechanisms such as carbon offsetting. Leading in circular business models can also create a brand halo effect, enhancing corporate reputation.

There can also be an opportunity to lead and collaborate on a cross-industry platform solution to register and administer e-waste certification. Such cross-industry collaboration approaches should strengthen supply chain partnerships, build resilience over the long term, and yield far greater industry influence for key collaborators.

And for value chain partners

For investees there are also clear benefits as this approach offers direct investment to build circular economy capabilities and decarbonize Scope 1 and 2 activities. They gain the ability to claim passive Scope 3 emission reductions and purchase validated Scope 3 emission claims while fostering stronger cross-industry collaborations.

But not without some challenges

Despite the clear benefits, certain challenges and industry dynamics must be addressed. For circular business models to thrive, the value of circular products must eventually reach parity and offset the value of (replaced) linear products. As circular volumes rise, upstream players — eg mining companies—may have concerns about reducing demand for virgin materials eg metal ores.

One critical success factor will be carefully negotiated agreements between value chain partners regarding the value and off-take of carbon certificates. These agreements must ensure a sustainable long-term model.

The path forward

The biggest winners in this space will be the ones who capitalise on investing in partners first, building the knowledge and credibility in their supply chains, and not only encouraging a circular economy but owning a stake in it – even leading it.

Baringa‘s experts in Telco, Supply Chain, and Sustainability can support you in understanding the potential circular opportunities for your business and in developing a bespoke strategy and circular industry blueprint. Contact us to explore how we can support your journey.

1. UN Global E-Waste Monitor, 2024, Link

2. PCB Today Sep 2024, Link

3. Lloyds Registry, May 2024, Link

4. Life Cycle environmental impacts of a smartphone, Ericssion, 2016, Link

5. Reuters, 2019 Link

6. Markets and Markets Research, 2024, Link

7. Refurbished Smartphone Market, FMI, Link

8. Canalys analysis, 2025, Link

9. Assessment of the environmental impact of a set of refurbished products, 2022,Link

10. Assumed 5% growth given varied market analyses ranging from 4.1% to 6.8%

Our Experts

Related Insights

Have we reached peak net-zero?

Why focused commercial collaboration is the route to net zero supply chains.

Read more

Value left on the table with circularity. Could an insetting revolution be the answer?

It is estimated that there is a multi-trillion-dollar global opportunity to reduce Scope 3 emissions. A revolution in approach for insetting could drive greater value from eWaste and circularity.

Read moreRelated Client Stories

Building a trusted data platform to enable scaling and cost savings

How do you accelerate delivery of a £multi-billion network expansion programme using advanced analytics and targeted insight?

Read more

Developing a Target State Operating Model for a technology and language services provider

Developing a comprehensive high-level target state operating model, defining the process architecture, and modelling the necessary capabilities for success.

Read more

Streamlining organisational structure to reduce complexity, scale, and grow

A new organisational resulted in a 10% cost efficiency across the organisation, as a result of simplification, standardisation, and the elimination of role duplication.

Read more

Enabling rapid, cost-efficient scaling of a nationwide fibre network build programme for a major UK telco

A major UK telco needed to heavily scale their nationwide fibre network build programme, with an ambition to deliver gigabit speed connectivity to over 7 million homes.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?