2025 Outlook: What lies ahead for climate and sustainability in financial services?

4 min read 15 January 2025

2024 brought significant change for sustainability professionals in financial services, not least through the results of elections in over sixty countries and the outcomes of a trifecta of UN Conferences of the Parties (COPs) on climate, biodiversity, and desertification.

As we look to the year ahead, here’s what is front-of-mind for myself and my colleagues, based on our dialogue with, and work for, sustainability leaders across financial institutions:

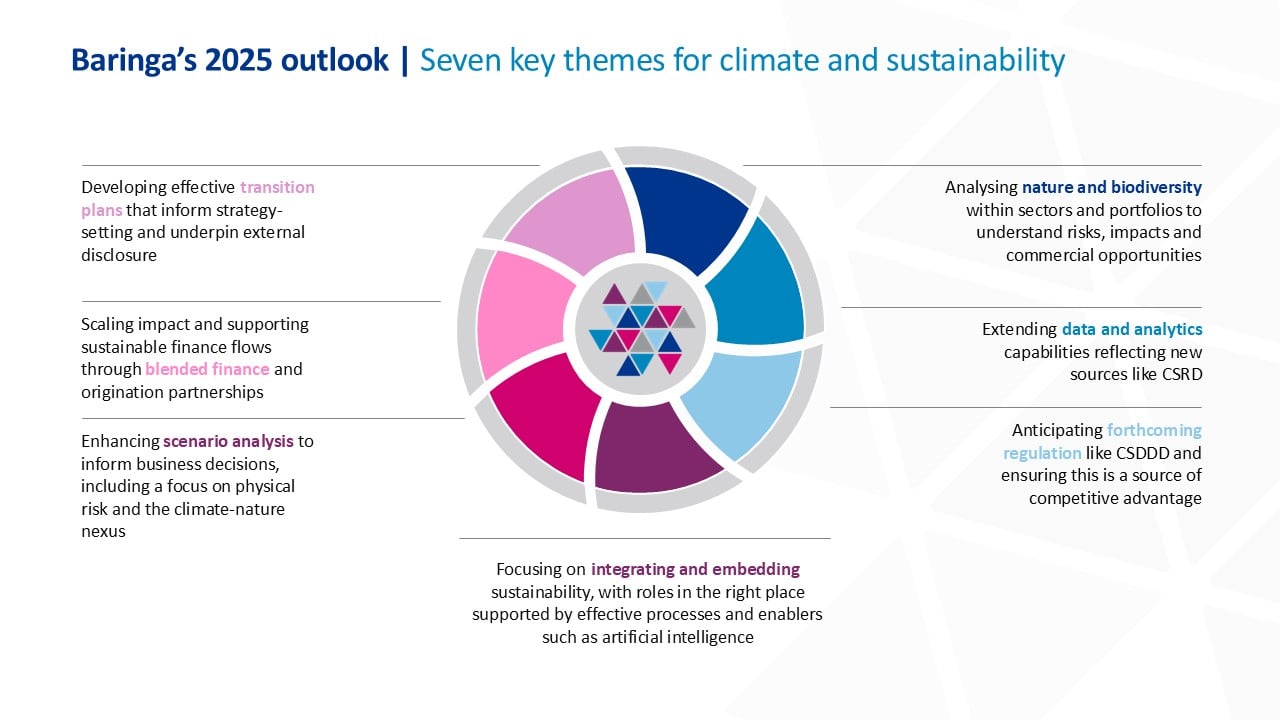

- Talking transition: Action continues to shift from a backward-looking ‘tell me’ style of disclosure to a forward-looking ‘show me’ approach, often in the form of a transition plan. These plans can be informed by regulation—such as the Corporate Sustainability Reporting Directive (CSRD)’s requirement to have targets, actions, and policies. But transition planning should be approached by financial institutions firstly as a vehicle for internal strategy-setting and planning, in the process forming the basis for external disclosure. Through this, financial institutions are well advised to broaden beyond climate mitigation and articulate their expectations, and the role they will play, on adaptation, social justice, and nature dimensions of the transition.

- Go where the money isn’t: Our 2024 outlook discussed the importance of defining transition finance, an area many made progress in. But even when defined, obstacles persist to the scale-up of climate solutions, including policy instability and heighted interest rates, constraining financial institutions’ ability to meet portfolio returns targets, sustainable finance commitments, and impact goals such as Net Zero targets. In response, financial institutions need to critically examine technologies and transaction structures, bringing in blended finance solutions and origination partnerships to help bridge financing gaps, risk-return mismatch, and support scalability. In doing so, there is potential to counteract declines in volumes of many traditional sustainable finance products, increase impact, and provide renewed impetus to sustainable finance teams.

- Scenarios, thinking fast and slow: With so many facets to the transition, firms’ approaches to scenario analysis will need to evolve. Informed by a continued focus on streamlining, sophisticated financial institutions will take time in 2025 to analyse plausible nature scenarios and the climate-nature nexus, as well as dialling up their physical risk analysis capabilities given the increasing severity of the near-term overshoot against the Paris Agreement and Net Zero emissions goals against which many firms have set portfolio targets. We expect 2025’s updates to the Prudential Regulation Agencies’ Supervisory Statement 3/19 to enhance approaches to scenario analysis amongst PRA-regulated institutions, potentially requiring this to be a more strategic exercise which also informs transition planning against most likely near-term outcomes.

- Not forgetting nature: WWF’s Living Planet report showed a continued decline in the state of biodiversity, even as agreement at the Biodiversity COP progressed efforts to integrate nature into economic systems with an agreement on ‘Digital Sequence Information’, which aims for businesses to contribute funding where they use genetic information from nature. Banks, investors, and insurers are developing increasingly sophisticated capabilities to assess where nature-related impacts and dependencies are already financially materially to the companies they provide financial services to, and where this may change over time. Scenario analysis and stress testing form a core part of these capabilities, used both for risk management and opportunity identification. 2025 will bring new product launches with a focus on private debt, nature markets and alternative investments—extending 2024’s significant growth in nature finance flows. But it will also bring continued expectation to manage nature-related financial risks with new requirements from Finma in Switzerland, and continued progress expected by the European Central Bank and European Banking Authority.

- Data everywhere, but where is the insight? For those captured by the Corporate Sustainability Reporting Directive (CSRD), recent years have been spent grappling with double materiality, datapoint availability, and how to structure CSRD disclosures alongside an already-complex landscape of integrated reports, ESG reports, TCFD disclosures, and more. But it’s possible to have overlooked the bigger implication—just as financial institutions are disclosing according to new frameworks including that of the Transition Plan Taskforce and ITPN, so are their investees or clients. Over the past decade, sustainable finance has been animated by the belief that with sufficient data, capital allocation can be tilted in favour of sustainable outcomes. While progress has to date been frustrated by conflicting frameworks, platforms and methodologies, CSRD has transformative potential. But in order to respond, financial institutions need to critically examine their data strategies, analysis capabilities and stewardship and engagement approaches so that they are positioned to receive, and act upon, increased quantities of increased quality data.

- More regulation: Sorry to say it—because I suspect everyone feels they’ve had to respond to plenty of regulation in recent years, but things aren’t slowing down. The centre of gravity continues to be the EU, where financial firms cannot ignore the Corporate Sustainability Due Diligence Directive (CSDDD) which sets a high bar for managing upstream value chain impacts—and potentially those from financing. We also expect significant progress toward International Sustainability Standards Board (ISSB) adoption in multiple jurisdictions—including via the UK’s Sustainability Reporting Standards—which has been overlooked by many financial institutions as they have prepared for CSRD. Firms would be well advised to also maintain a focus on compliance with existing and recent regulation, given increasing focus on enforcement. This includes greenwashing, with recent cases in multiple jurisdictions and more expected in 2025.

- More integration: Given the explosive growth in expectations, commitments, and regulation, financial firms have added significant headcount on climate and sustainability in recent years. It is critical they periodically step back and validate their objectives and role in solving societal challenges, and the resources they have dedicated to this. For some time now, financial institutions have been redistributing sustainability roles from centralised ‘group’ teams, out across functions and divisions. We are seeing a range of newer factors inform these decisions, such as the role artificial intelligence can play and how enhanced sustainability systems and processes—often driven by finance for reporting and assurance purposes—can help collaboration between teams. Alongside this comes a focus on where sustainability responsibilities can be integrated within wider roles; this brings with it a significant focus on capability building and how role-specific skillsets can be developed by those integrating sustainability responsibilities into their roles.

We’d love to hear your thoughts; if you’d like to discuss our perspectives in more detail please get in touch.

Our Experts

Related Insights

Future-proofing climate disclosures: Leveraging climate reporting for nature

Forward-thinking companies are integrating climate and nature into their strategies to drive innovation and resilience.

Read more

Transition planning in turbulent times: How financial institutions can adapt and lead

The shift to a low-carbon economy is challenging for financial institutions; we explore how they can adapt and lead in today's tough landscape.

Read more

Simplification Omnibus: what you need to know and where to go from here

We share what the Simplification Omnibus means for CSRD, CS3D and the EU Taxonomy and how you should respond.

Read more

Four steps to prepare for CSRD and the niche challenges for wealth and asset managers

We outline four steps financial institutions should take to tackle CSRD reporting and highlight specific considerations for wealth and asset managers.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?