Future-proofing climate disclosures: Leveraging climate reporting for nature

4 min read 23 March 2025

Australian businesses are built on nature—nearly half of its Gross Domestic Product (GDP) (A$900bn) relies on healthy ecosystems. As nature declines, risks rise from supply chain disruptions to soaring costs and operational hurdles.

Climate and nature are two sides of the same coin, each accelerating the other. Forward-thinking companies are integrating both into their strategy—not just to manage risk, but to drive innovation and long-term resilience.

Nature-related reporting isn’t mandatory yet, but it’s coming. The International Sustainability Standards Board (ISSB) has flagged it as a priority, and momentum is building fast. Businesses that move now will be ahead of the curve, future-proofing their operations and securing a competitive edge.

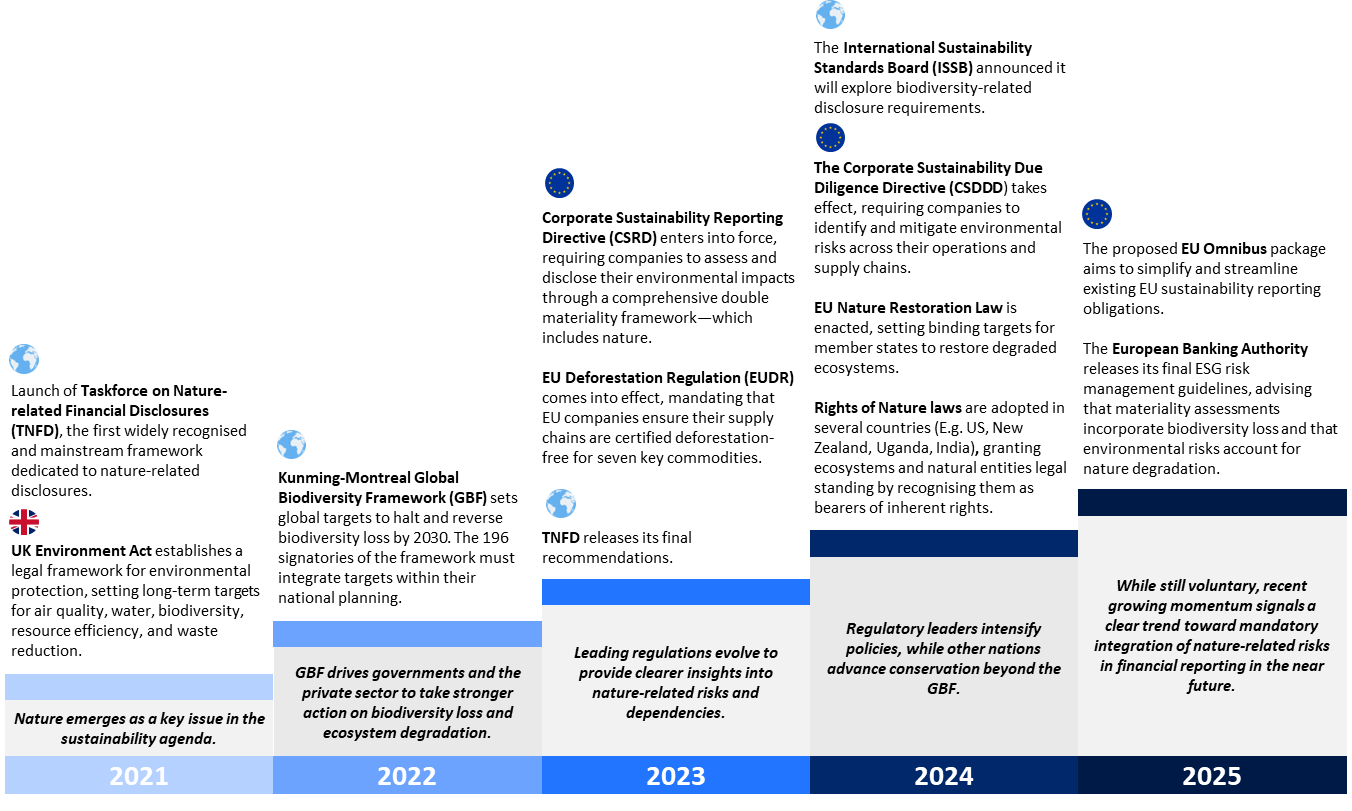

Mandatory nature disclosures are on the horizon

Australia’s mandatory Australia Sustainability Reporting Standard (ASRS) S2 climate reporting kicks in next year, aligning with ISSB standards and raising the bar for corporate transparency. The Australian Accounting Standards Board (AASB) is taking a climate-first approach, with nature soon to follow—mirroring the Task Force on Nature-related Disclosures (TNFD) push to integrate climate and nature risks into financial disclosures. The ISSB is also exploring nature-related standards.

Firms like Telstra and Bank Australia are already embedding TNFD principles into their climate reporting, setting a new benchmark. The momentum is clear: just as climate regulation surged, nature is next. Businesses need to be ready.

The momentum of global nature-related frameworks and regulation

Source: Baringa

No regrets actions to future-proof your disclosures

The good news? Organisations that get ahead now—by embedding nature into their ASRS S2 compliance—will future-proof their reporting, streamline processes, and sidestep costly administrative headaches later down the track. Taking "no regrets" actions now—aligning with ASRS S2—will ensure a seamless transition when nature-related disclosures become standard:

1. Conduct a nature capability assessment to understand readiness for nature-related reporting elements.

As with climate reporting, start by assessing your existing capabilities—such as expertise, data, and processes—and map these against the desired capability level for nature-related reporting. This gap analysis helps identify areas for improvement, allowing you to create a targeted plan for building capacity, enhancing data quality, and integrating nature considerations into your business strategy, based on the processes and experience gained through climate assessments.

2. Ensure double materiality assessments encompass both climate and nature-related financial risks, dependencies, and impacts, identifying your most material nature challenges.

These insights, gathered before disclosure, equip leadership teams to make strategic decisions on natural capital risks and opportunities, integrating nature alongside climate into governance and strategy to meet net-zero and nature-positive targets.

3. Conduct integrated climate-nature scenario analysis.

Leverage the climate scenario analysis frameworks you have in place to integrate nature into the process, especially where there is a strong connection between climate and nature physical risks such as for water availability. Failing to capture nature in climate scenario analysis can create risk for an organisation by potentially underestimating the full extent of climate change impacts.

Comprehensive climate-nature scenarios are some way off - but organisations can use tools like the TNFD toolkit to establish a consistent organisational view on likely future pathways and use this as the basis for risk quantification under likely and extreme scenario outcomes.

4. Identify the risk and opportunity management elements that need adjusting to integrate nature-related risks into your enterprise risk management framework.

To effectively incorporate nature-related risks, draw on insights from your climate risk assessments to identify areas where your existing risk management processes can be adapted. Ensure alignment between climate and nature risks within strategic planning, governance, and key stakeholders. The TNFD’s five integration principles provide a valuable framework to embed nature into existing risk management strategies.

5. Once you’ve assessed your current position, define your desired nature ambition state.

Consider whether to take a proactive approach by embedding nature into your strategy and operations or to align with industry developments, adapting as regulations and expectations evolve. By leveraging your experience and procedures in setting climate targets, you can begin to explore and shape your nature ambition in a way that aligns with your organization’s readiness

6. Disclose the nature-related metrics most material to your business, aligning them with measurable targets and transition plans—just as you do with climate emissions metrics.

Internal actions, such as monitoring frameworks and data tracking, can help inform these disclosures by providing the necessary insights and ensuring accuracy. Use TNFD metrics as a benchmark to refine and strengthen your internal processes, which, in turn, can support more robust and transparent disclosures. For example, organisations where deforestation is material may begin with metrics to identify risks, refine monitoring approaches, and assess the need for policy integration.

Baringa has worked with several organisations to get them ASRS-ready and build robust disclosure practices, while also supporting them as they tackle emerging nature challenges.

Find out how we help our clients in Climate Change and Sustainability.

Our Experts

Related Insights

Transition planning in turbulent times: How financial institutions can adapt and lead

The shift to a low-carbon economy is challenging for financial institutions; we explore how they can adapt and lead in today's tough landscape.

Read more

Simplification Omnibus: what you need to know and where to go from here

We share what the Simplification Omnibus means for CSRD, CS3D and the EU Taxonomy and how you should respond.

Read more

2025 Outlook: What lies ahead for climate and sustainability in financial services?

Here's what's front of our minds for 2025 based on our dialogue with, and work for, climate and sustainability leaders across financial institutions.

Read more

Four steps to prepare for CSRD and the niche challenges for wealth and asset managers

We outline four steps financial institutions should take to tackle CSRD reporting and highlight specific considerations for wealth and asset managers.

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?