Balancing investor demands, offtake opportunities and competitiveness in Australian Storage CIS tenders

5 min read 14 July 2024

The Capacity Investment Scheme (CIS) is a Commonwealth Government vehicle to underwrite new renewable energy and storage assets via Capacity Investment Scheme Agreements (CISAs). The CIS seeks to support delivery of 23 GW of generation and 9 GW of storage capacity by 2030.

Given the potential scale of this scheme over the next five years, every storage market participant needs to refine their strategy, governance, and bid approach to account for the market’s new largest buyer of storage contract agreements.

Baringa supports clients in building competitive bids that meet internal return requirements through detailed assessment of project fundamentals, market price outcomes and competitive dynamics. Our modelling shows that a wide range of bid strategies can be successful, provided the critical Annual Payment Cap is managed.

Storage tender rounds are expected to remain highly competitive, with battery capacity under development exceeding tender volumes.

The first CIS auction, the South Australia-Victoria Tender for battery storage capacity, saw significant investor interest. The massive over-subscription for the 2,400 MWh tender reflects the strong pipeline of storage projects across the two states.

We expect near-term storage tender rounds to be similarly competitive, driven by relatively low barriers to constructing battery assets in the National Electricity Market (NEM) and the depth of high-quality development assets in the market. Further, if the next Storage CIS tender rounds apply the unique back-dated project eligibility threshold for New South Wales (NSW) (committed from November 2019) relative to the rest of the NEM (committed from January 2024), we expect to see more mature NSW battery projects enter future NEM-wide tenders.

The design of the CIS makes it a flexible tool for risk management

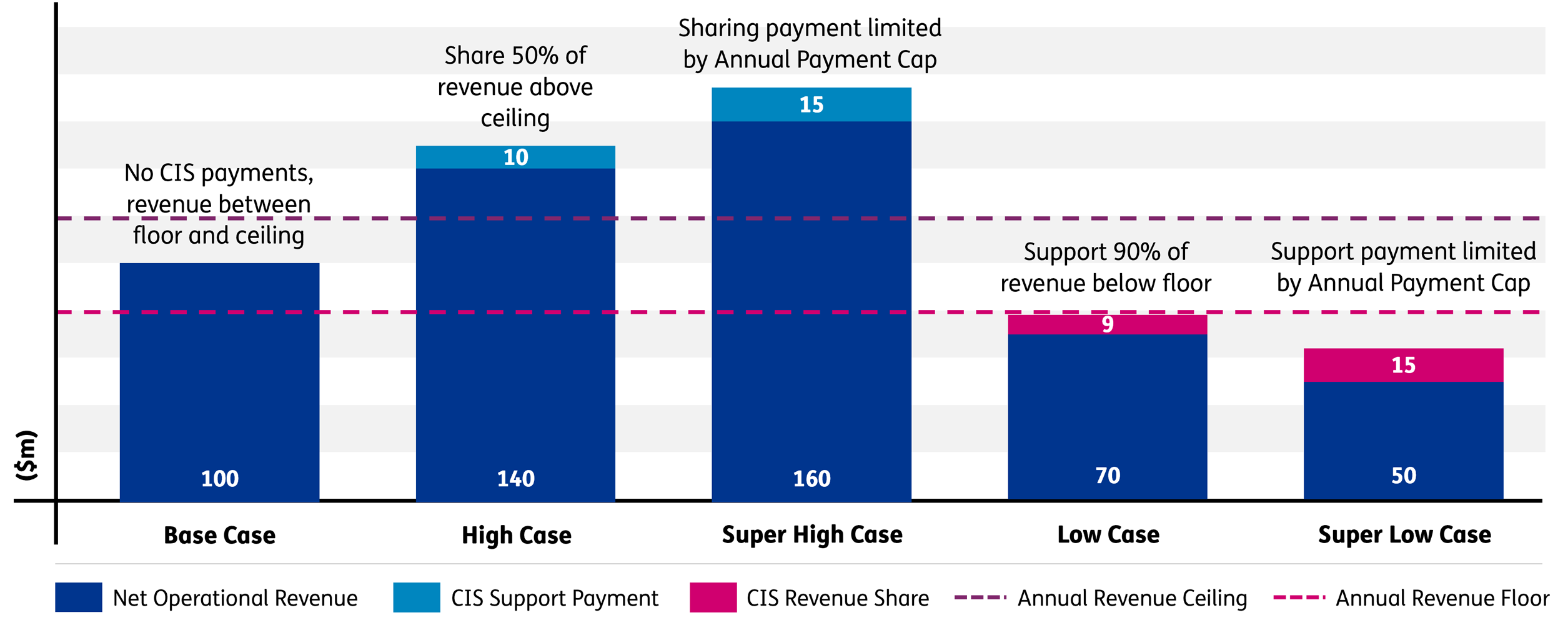

The CISA is designed to provide bidders with greater certainty over their projected revenues for up to 15 years. It is the responsibility of the proponent to determine what they require of the CISA (e.g. “top up revenue” vs “protect against a wholesale market downturn”).

The contract is structured such that 90% of any shortfall below a bid Revenue Floor is paid to the project by the Commonwealth, while 50% of any revenue above the bid Revenue Ceiling is returned to the Commonwealth. Both payments are capped by an Annual Payment Cap. Bid variables including the Revenue Floor, Revenue Ceiling, and Annual Payment Cap can vary year on year, enabling proponents to tailor their bid.

The figure below illustrates how CIS support payments and revenue share payments interact with a given level of Net Operational Revenue under a spread of outturn market price scenarios. It also highlights the role of the Annual Payment Cap, set at $15mn in this example, in limiting contractual exposure to both the proponent and the Commonwealth.

Illustrative asset revenue scenarios and interactions with CIS

Source: Baringa

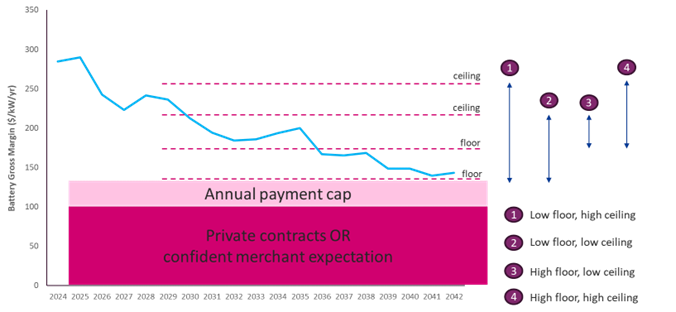

Successful bidding strategies will not be uniform, meaning detailed analysis is needed to understand the landscape.

The strategic objectives and risk tolerance of investors result in a variety of bidding approaches, ranging from seeking downside protection for debt service requirements to supporting equity.

As the bid variable that drives maximum liability to the Commonwealth, the Annual Payment Cap is likely to have the most influence on bid competitiveness.

Bankable commercial contracts at market rates also provide the bidder more flexibility to adjust their Annual Payment Cap (effectively limiting liability to the Commonwealth Government) while maintaining a Floor that delivers a target hurdle rate.

Illustrative example of different bid strategies

Source: Baringa

A clear market outlook of both merchant prices and offtake prices is integral in determining the optimal bid strategy. This allows proponents to shift underwriting value to when it is most required, inform strategic decisions on when to accept higher merchant exposure (or structure commercial contracts), understand the resilience of returns to a variety of credible market scenarios, and, ultimately, maintain a competitive bid from the perspective of the Commonwealth.

Project fundamentals remain important

Baringa considers three project fundamentals that influence the competitiveness of a storage project in the CIS:

- CAPEX efficiency: capital savings remains a key driver of cost-competitiveness. Investors who can capitalise through portfolio scale, OEM pricing, or synergistic benefits achieved through co-location of assets will all drive favourable unit capex costs.

- Cost of capital: hurdle WACC is important in determining the price floor, noting that this will vary by developer.

- Revenue certainty: sufficient private contracting is essential to gain confidence in market revenue streams, which in turn places downward pressure on Annual Payment Cap.

Bidders need to be adaptable to tender changes

Interestingly, the most recent CIS Tender 1 for NEM-wide generation assets included two key terms that were not previously included in the South Australia-Victoria Tender:

- Related entity contracting: the CIS provides underwriting based on a project’s Net Operational Revenue, inclusive of revenues earned under bilateral contracts and merchant operations. However, wholesale contracts with a related party will be valued using wholesale spot market prices. This is likely to impact gentailer developers, who will need to mitigate the risk of two swap contracts during high-priced wholesale years.

- Opt-out periods: Operators can opt out of CISA revenue support arrangements for 5-year periods. This provides additional flexibility for operators to capture a larger proportion of upside returns in the medium-term while retaining support in the long-term.

It is not yet confirmed if these terms will be introduced into future storage tenders or will remain only for generation tenders.

Baringa has supported investors in both the NEM and the WEM on over 100 project financing transactions to date. We help our clients to identify which technologies to invest in, the locations with the most potential, and the optimum timing of entry. Our team also specialises in bid strategy development and wholesale risk management, assisting clients with market and commercial advice into centralised tender processes.

Find out more about our NEM Reference Case, and the risks and opportunities for investment, by contacting one of our experts below.

Our Experts

Related Insights

Synchronisation of the Baltic power system with Continental Europe opens exciting opportunities for batteries

The synchronisation of the Baltic power system with continental Europe is a significant milestone that opens exciting opportunities for batteries.

Read more

Renewables Market Scanning Report

Which are the most attractive markets for investing in renewable assets globally?

Read more

How can investors and developers capitalise on South Korea’s evolving energy market?

South Korea's energy market is transforming in line with the global shift to renewable energy.

Read more

How ‘Equipment-as-a-Service’ models unlock commercial decarbonisation

Read our latest piece, created in collaboration with Tallarna, to explore the components of an ‘Equipment-as-a-Service’ model, how they can be deployed, and how to increase take-up.

Read moreRelated Client Stories

Shaping New Zealand’s energy transition conversation

How do you create a distributed energy model that draws on best practice from around the world but is also fit-for-purpose for New Zealand?

Read more

Electricity network operator: securing critical national infrastructure with hybrid defences

Breaking new ground with a hybrid security approach.

Read more

Maximising impact from AI investment for a global energy leader

Discover how a series of experiential learning events resulted in employee confidence in AI skills hitting 85%.

Read more

Maintaining the stability of the New South Wales power system

How do you ensure the future stability of the NSW power system?

Read moreIs digital and AI delivering what your business needs?

Digital and AI can solve your toughest challenges and elevate your business performance. But success isn’t always straightforward. Where can you unlock opportunity? And what does it take to set the foundation for lasting success?